Introduction to Insurance

Insurance is a financial tool that provides protection against unexpected risks and losses. It helps individuals and businesses safeguard their assets, health, and financial stability by transferring risks to an insurance provider in exchange for regular premium payments.

Learning Outcomes

- Understanding risks and perils

- Learning about savings and investment

- Knowing about concept of insurance

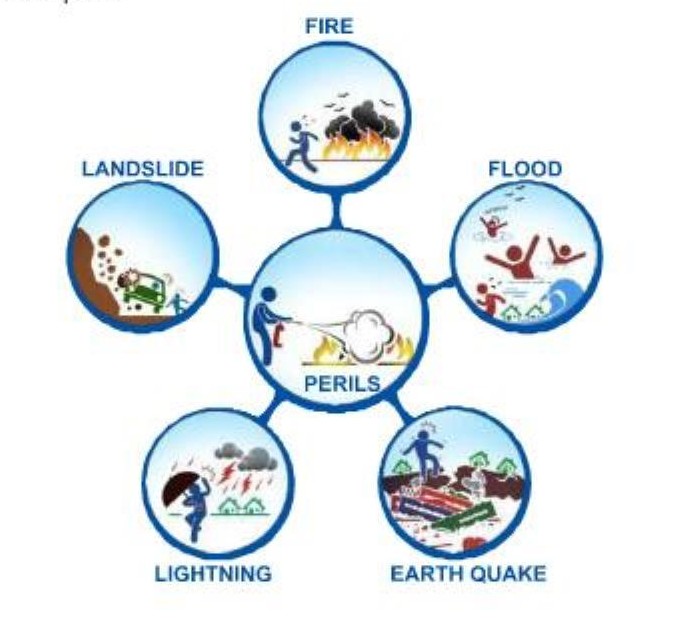

1. Risk and Perils

Every day, we hear stories about accidents and other misfortunes that someone has suffered.

Some of these include:

- All of a sudden, peoplefall seriouslyill.

- Motor vehicles are stolen and people die or get injured in accidents involving motor vehicles.

- House and belongings are destroyed by fire.

- Large scale loss of lives and destruction of property in cyclones and tsunamis.

Life is full of uncertainties and surprises. Protecting oneself, one's families and society from these uncertain events has beenoneofthe biggest concerns of man for centuries.

Definition

‘Risk’ is a term that we use to refer to the chance of suffering a loss as a result of uncertain events like the above.

The events that give rise to such risks are knownasperils.

Some examples of perils:

We face many suchrisks in our day-to-daylife including risks to ourlife, health, property and soon.

We don't know whether and when something unfortunate will happento us or our family members or property. It may not always be possible for us to prevent such a happening. For instance, we cannot prevent a storm or somebody's death from occurring.

2. Savings and investment

It is possible for us to take measures to reduce the financial consequencesthatarise due to the above mentioned risks and protect ourselvesfinancially. One of the ways by whichthis is normally doneis with the help of savings and investment.

Example

We would have seen or learnt from our parents or elders about the need to save for the future. By saving or investing money, the money so accumulated can be used to cope with the loss. However, such savings can only give back our own money plus somereturns.

What would happen if a human life is lost or a person is disabled permanently or temporarily?

Example

A person dies suddenly. Where would the person's family get the money from to support itself? How would the person's family meet the variousliving expensesafter his death?

A person suffers a paralytic stroke that leaves him permanently bed- ridden. Such an event would result in loss of income to the household and put the family in a lot of hardship.

The loss suffered Is so large in all such situations that one’s savings may not be sufficient to take care of the financial burden.

3. Insurance

Luckily for us, there is something called 'Insurance’. It is founded on a simple idea. Even though an eventlike death or a fire can come as a terrible economic blow to someone, when we take the society as a whole, during any given year, only a few would suffer in such manner. Ifa small contribution is collected from everyone in the community and pooled to create a common fund, the amount so pooled can be used to pay money to the few unfortunate members who have been subject to the loss.

Definition

Insurance is a mechanism of risk transfer and sharing by pooling of risks and funds among a group of individuals who are exposedto similar kindsof risks for the benefit of those who suffer loss on accountofthe risk.

Insurance is, thus, a financial tool specially created to reduce the financial impact of unforeseen events and to create financial security. Indeed, everyone who wants to protect himself against financial hardship should considerinsurance.

Traditionally, “the joint family” has been an informal social security in India. In modern society, social security is available only to those who are employed in the organized sector. Insurance is considered one of the tools of social security for formal and Informal sectors and is largely carried out in two ways.

-

The first way is known as Social Insurance. Here, the State or government takes care of those who are subjected to losses due to some risk event. Examples are, providing a pension when one grows old or providing free medical treatment, meeting the cost of hospitalization etc. The fund for this purpose comes from a pool made up from taxes or mandatory social security contributions required to be made byall those who work and earn an income. The Employees’ State Insurance scheme (ESI) that provides medical care and other benefits to employees and Employees’ Provident Fund Organization (EPFO) that provides pensions and survivors' benefits in the event of an employee's death are the popular schemes underthis head.

-

The second way is through voluntary Private Insurance. Here, individuals and groups can buy insurance from an insurance companybyentering into a contract of insurance with the company. The insurance company enters into a contract (an insurance policy) whereby it (insurer) undertakes, in exchange for a small amount of money (premium), to provide financial protection by agreeing to pay the insuring person (insured) a fixed amount of money (sum assured) on the happening of a certain event(insured peril).

Insurance companies collect premiums to provide for this protection and losses are paid out of the premiums so collected from the insuring public. In other words, an insurance contract promises to make good to the insured a certain sum in consideration for the premium received from the insured.

Example

The following two examples explain the concept of insurance

Example 1

In a village, there are 400 houses, each valued at Rs.20,000. Every year, on an average, 4 houses get burnt, resulting into atotal loss of Rs.80,000.

| Number of houses | 400 |

| Value of each house | Rs. 20,000 |

| Houses that get burnt every year (average) | 4 |

| Total loss (4 houses X Rs. 20,000) | Rs. 80,000 |

| Contribution to be made by 400 house owners to compensate for loss of Rs. 80,000 = Rs, 80,000 / 400 | Rs. 200 |

If all the 400 owners come together and contribute Rs.200 each, the common fund would be Rs.80,000. This is enough to pay Rs.20,000 to each of the 4 owners whose houses got burnt. Thus, the risk of 4 owners is spread over400 houses/ house-owners of the village.

Example 2

There are 1000 persons, whoareall aged 50 and are healthy.It is expected that of these, 10 persons may probably die during the year. If the economic value of the loss suffered by nehgaeach dying person is taken to be Rs.20,000, the total loss would work out to Rs .2,00,000.

| Number of houses | 1000 |

| Economic value of each person | Rs. 20,000 |

| Persons that may die during the year (probable) | 10 |

| Total loss (10 persons X Rs. 20,000) | Rs. 2,00,000 |

| Contribution to be made by 1000 people to compensate for loss of Rs. 2,00,000 = Rs. 2,00,000 / 1000 | Rs. 200 |

lf each person of the group contributes Rs.200 a year, the common fund would be Rs.2,00,000. This would be enough to pay Rs.20,000 to the family of each of the ten persons who may die. Thus, 1000 persons sharetherisk of loss due to death suffered by 10 persons.

From the above,it can be seen that insurance is a very useful financial tool for pooling, sharing and transfer of the risk so that the financial loss caused to a person whosuffers due to aperil is compensated.

Case study: Risk and Protection

Sheetal and Simran are friends from the same class and regularly go home together. Sheetal always carries an umbrella and Simran makes fun of her. Sheetal simply smiles and says that as the umbrella protects her from sun and rain, she does notfeel it to be an additional burden to carry along with text books in her school bag.

One day, it suddenly started raining. Simran did not get either raincoat or umbrella because of which she got wet as did her bag and books. Sheetal used her umbrella to protect her and her bag from rain. Sheetal offered to share her umbrella and asked Simran to come to her house. After reaching Sheetal's home, Simran found that Sheetal's father was carefully sorting out a bunch of papers and making notes. Sheetal's mother had refreshments arrangedforall of them, without making much noise. When Simran asked Sheetal's mother why uncleji was so serious, she said, “Actually, your uncleisfinalising papers for purchase of an insurance policy’.

“Whatis an insurance policy,” Simran enquired.

Sheetal's mother explained, “Insurance offers protection against unforeseen risks,just like a raincoat or umbrella protects you from rain.

"What is a risk?" Simran asked.

Sheetal's mother said, “See Simran, we face manyrisks in ourlives. For example, if you drench yourself in rain, you mayfall sick. There is a risk ofillness. Due to rain, there could be a short circuit of electricity. There is a risk of electronic breakdown of this TV as well as other domestic appliances. There is a risk of theft of our car which is parked in the garage andthere is alsothe risk of an accidentwhile crossing the road.

So risk is an inherent part of ourlife. Whether and when loss would be caused because of risk and how much loss is caused cannot be foreseen, knownor controlled at all times. While we cannot avoid most of these risks, by purchasing insurance, we can transfer the riskto the insurance company.”

Simran asked, “Howdoesthis happen”?

Sheetal's mother explained, “Suppose the downpouris heavy resulting in a! lood, our car could get immersed in water. It could damage a few vital parts necessitating repairs. Since we have insured our car, the insurance company will reimburse the expenses of repairs, thereby reducing the impact of loss becauseof damagetothe car." Simran asked innocently, “But aunty, why cannot the rain be stopped” and then, she sneezed. Sheetal’s mother exclaimed, ‘Bless you!’ and told her, “Had you taken an umbrella you could have protected yourself from getting wet. See, now since you got wet, can we stop you from sneezing"?

Everyone laughed.

Your comments