Insurance Sector in India

India's insurance industry is a fast-expanding sector that serves as an integral part of financial security and risk management. The industry is regulated by the Insurance Regulatory and Development Authority of India (IRDAI) and comprises life insurance, general insurance, health insurance, and reinsurance services. The sector is dominated by public and private insurance companies that provide a variety of policies that are designed according to individual and corporate requirements. With growing financial literacy, government schemes such as Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Ayushman Bharat have increased insurance penetration. The industry is still transforming with digital innovations, and insurance is becoming more accessible and efficient in urban and rural India.

Learning Outcomes

- Understanding regulatory framework

- Knowing about IRDAI's role and functions

- Learning about insurers, intermediaries and other institutions

1. Understanding Insurance sector in India

a. Insurance regulation In India

- The Government began to exercise somesort of control on insurance business by passing the Life Insurance Companies Act and the Provident Fund Act in the year 1912.

- Thereafter, based on the changing requirements of the industry, a comprehensive legislation, The Insurance Act, 1938, was passed followed by subordinate legislation including Insurance Rules, 1939.

- This Act was further extensively amended in 1950 and there after in 1999 when the IRDAI Act, 1999 wasintroduced.

- Someother existing legislations in the field are — the Life Insurance Corporation (LIC) Act, 1956, the Marine Insurance Act, 1963, General Insurance Business (Nationalization) Act, 1973, Motor Vehicles Act, 1988, the Redressal of Public Grievances Rules, 1998 framed by Central Government with regard to Insurance Ombudsman etc. Provisions of the Indian Contract Act, 1872 are applicable to the contracts of insurance and some of the provisions of the Companies Act, 2013 (previously Companies Act, 1956), are applicable to the companies carrying on insurance business.

- Insurance Regulatory and Development Authority of India (IRDAI) On 6th January 2000, the President of India gave his assent to the Insurance Regulatory and Development Authority Bill, which enabled opening up of the insurance sector to private players. The Insurance Regulatory and Development Authority of India (IRDAI*) Act, 1999 facilitates the establishment of Insurance Regulatory and Development Authority as an autonomous regulatory body for the Indian insurance industry. Accordingly, on 19th April, 2000, Insurance Regulatory and DevelopmentAuthority of India (IRDAI"), was created under the IRDAI* Act, 1999 to regulate, promote and ensure orderly growth of the insurance industry and to protect the interests of policy holders.

Some of these Acts are underthe process of revision as well.

Composition of IRDAI

The Authority consists of a

- A Chair person

- Five whole-time members and

- Four part-time members

Functions of IRDAI

Functions of IRDAI

- Toprotect the interests of holders of insurance policies;

- Toregulate, promote and ensure orderly growth of the insurance business and reinsurance business.

IRDAI issues certificate of registration to insurance companies and licenses to all intermediaries who are engaged In insurance related activities. IRDAl makes regulations for the various institutions’ entities operating in the insurance industry and supervises compliance with these regulations through returns and inspection. IRDAIalso facilitates resolution of complaints against insurance companies.

As apart of its developmental role, IRDAI emphasizes on empowering public through policyholders’ education, which helps to increase the insurance reach for the benefit of common man. It has adopted multipronged approach for educating consumers and organizes Insurance Awareness campaigns directly and through industry promoting insurance education acrossthe country.

b. Indian insurance market

After opening up of the insurance sector in 2000, a number of private players entered Indian insurance market increasing the competition among Insurers for the benefit of consumers.

- By 2014, the insurance industry of India consisted of 52 insurance companies of which 24 are in Life insurance business and 28 are Non-life insurers.

- Among Life insurers, Life Insurance Corporation of India (LIC) is the sole public sector company.

- Out of 28 Non-life insurance companies, there are six public sector insurers of which two are specialized insurers namely, Export Credit Guarantee Corporation of India for export credit insurance and Agriculture Insurance Company of India Ltd. for crop insurance. Four private sector insurers are registered to exclusively underwrite policies in Health, Personal Accident andTravel insurance segments.

- In addition to these, there is a sole national re-insurer, namely, General Insurance Corporation (GIC) of India

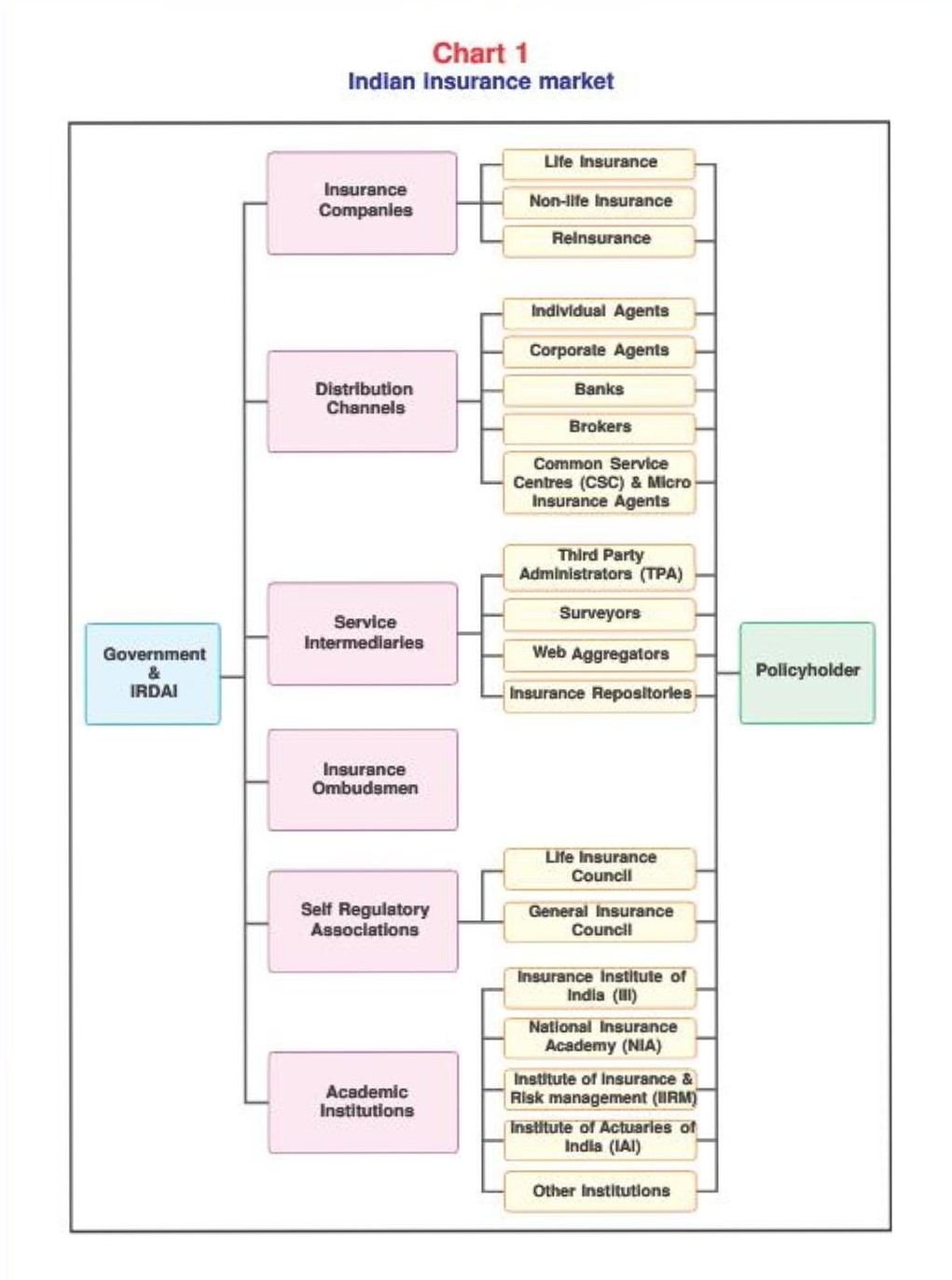

2. Other institutions in Indian Insurance Market

In addition to the insurers, there are other institutions which are operating in the Indian insurance market.

a. Distribution channels and other Intermediaries

- Intermediaries involved in distribution of insurance products are agents (individual, corporate and micro-insurance), brokers, web aggregators, Common Service Centers.

- Intermediaries like surveyors and loss assessors are involved in claim assessment of general insurance.

- Specialized intermediaries for health services called Third Party Administrators (TPAs) operate in Health insurance for issuance of policy cards, for organizing cash less treatment facility through network of hospitals, handling and settlement of claims.

- Insurance Repositories are intermediaries introduced recently to electronically maintain data of insurance policies for ease in storage, retrieval and servicing of insurance policies.

b. Insurance Ombudsman

In case a grievanceof a policyholder is not redressed by the insurer, alternate grievance redressal mechanism is provided for in the insurance sector through the institution of Insurance Ombudsman set up under the Redressal of Public Grievance Rules, 1998.

Subject matter of complaints that can be taken up before Insurance Ombudsmen are partial or complete repudiation of claims and delay in settlement, non-issuanceofpolicy, dispute relating to premium and interpretation of clauses in relation to claim. There is no provision for appeal against the order of Ombudsman under the Redressal of Public Grievances Rules. If not satisfied, the policyholder or claimant may ignore the award and go to the court, consumer forum etc., and if the customer consents, the insurer is has to implement the award unless it chooses to approach Court.

c. Self-Regulatory Institutions

Self-regulation in insurance is through the Life insurance council and the General insurance council. These Councils include all registered life and general insurance companies as their members respectively and are statutory bodies constituted under the Insurance Act, 1938.

d. Training Institutions

As the various intermediaries in insurance sector have to fulfill specific requirements of eligibility like training and passing of examinations,training institutions form an important part of the Insurance Sector. Institutions like Insurance Institute of India, National Insurance Academy, Indian Institute of Insurance and Risk Management, Institute of Actuaries of India, Agent Training Institutes, etc. provide training, conduct examinations andprovide professional manpowerforthe insurance sector.

Your comments