Principles of Insurance

Insurance is founded on basic principles that guarantee fairness, trust, and financial security for all stakeholders. These concepts are Utmost Good Faith, whereby both insurer and insured should reveal all facts truthfully; Insurable Interest, by which the policyholder has to have an interest in money terms in the insured property or person; and Indemnity, to ensure insurance covers only genuine loss, avoiding pecuniary profit from a claim. Some other important concepts are Contribution, Subrogation, and Proximate Cause, which assist in resolving claim settlements and liability. Knowledge of these principles is required for informed decision-making regarding insurance policy terms and coverage

Learning Outcomes

- To know that insurance follows law of large numbers

- Knowing what is Insurable interest

- Knowing that Utmost good faith operates in Insurance Contracts

- Understanding Indemnity

- Learning about Subrogation and Contribution

- Understanding Proximate cause

The principles of insurance are:

- Law of large numbers

- Insurable interest

- Utmost good faith

- Indemnity

- Subrogation and contribution

- Proximate cause

1. Law of large numbers

Imagine that in a village there are 1000 persons who are all aged 50 and are healthy. Based on previous experience,it is expected that of these, 10 persons may die during the year.If the economic value of the loss suffered by the family of each dying person Is taken to be Rs.20,000, the total loss would work out to Rs.2,00,000. If each member contributes Rs.200 a year, this would be enough to pay Rs.20,000 to the family of each of the ten persons who dies. You would have wondered whether the prediction of number of actual deaths of ten is accurate. What would be the impact if the insurance company's predictions about the risk turned out to be wrong or inaccurate and the number of deaths turns out to be 15 or 5? If the actual number of persons whodie during a year were to be higher than ten, the amount collected would not be sufficient to compensate those who suffer the loss.

You need not worry too much about the accuracy of estimates. What saves the insurer is a wonderful principle of nature known as the law of large numbers. Simply put, it states that the more the number of members who are insured, the more likely it is that the actual result would be closer to the expected.

Example

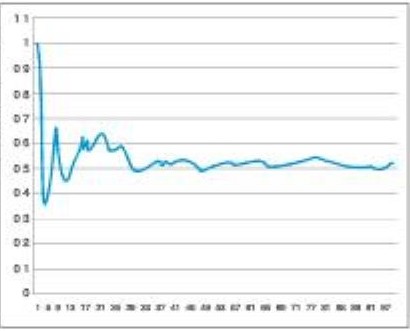

Try this simple experiment. Toss one rupee coin. We all know that the theoretical probability that the outcome will be 'heads' is equal to /2 Does this mean that if you toss a coin four times you will always get two heads and two tails? When can you be hundred percent sure that you will get heads exactly half the time? The answer is, you would have to toss it a very large number of times. You would also notice that the more number of times you toss the coin, the more you would find that the result is coming closer to half.

Law of large numbers - Number of tosses of a coin

Insurance works on this law of large numbers Insurance companies are able to make near accurate predictions about their risks because they typically spread that risk amongst thousands even millions, of members who have signed, contracts with them and who are their policy holders.

This is the reason why when you purchase an insurance policy, the insurance company is able to give you an assurance that your losses would be compensated if they occur due to the insured event.

2. insurable Interest

Another important principle is insurable interest. Let us understand it with the help of a few examples.

Example 1

Shri Manoj was staying with his wife and son. An insurance agent visited him offering health insurance. Manoj indicated that he wanted to take health insurance for all the members of his family. He also wanted to take a policy for his good neighbour. The insurer said that Manoj can take a policy for his family but cannot take a policy for his neighbour.

The reasons why the insurer refused to issue insurance policy to Manoj's neighbour was because Manoj did not have an insurable interest in his neighbour's health.

Insurable interest is the term we use to describe the relationship between the insured and the subject matter of insurance (in the above case it is the health of Manoj and his family on one hand and Manoj's neighbour). This relationship gives Manoj a particular type of interest in the health of himself, his wife and child, whereby he benefits from the good health and suffers a financial loss by way of hospital expenses if one of the members of his family falls ill. We buy insurance to ensure that the loss suffered is compensated for in some way. The position is not so in case of Manoj's neighbour as Manoj does not suffer any financial loss due to his neighbour falling ill.

Insurable interest exists when an insured person derives a financial benefit from the continued existence of the insured object or suffers a financial loss from the loss of the insured object. A person has an insurable interest in something when loss-of or damage-to that thing would cause the person to suffer a financial loss.

Example 2

If the house you own is damaged byfire, you suffer a financial loss resulting from the fire. By contrast, if your neighbor's house, which you do not own,is damaged byfire, you may feel sympathy for your neighbor but you have not suffered a financial loss from the fire. You have an insurable interest in your own house, but notin your neighbor's house.

Imagine that you had insured your house. Later you sold the house to buy a bigger house. There was fire in the house after you sold the house. Since you do not own the house anymore, you will not suffer any loss. Therefore, now you do not have any insurable interest in the house. Insurable interest should be there at the time the loss is suffered.

People have an insurable interest intheir property to the extent of loss suffered, but not more. The principle of indemnity dictates that the insured is compensated for a loss of property, but is not compensated for more than what the property was worth. A lender, who gives loan against the security of house, has an insurable interest on the property because if there is a loss to the house, he would suffer a loss by not getting back the money. However, the insurable interest of the lender is not in excess of the value of the loan.

3. Utmost good faith

While ordinary commercial contracts are good faith contracts, insurance contracts are contracts of utmost good faith. Let us distinguish between good faith and utmost good faith with the help of example.

Example

Example 1: You have accompanied your parents to a car showroom where they sell cars. Your father asks the salesman certain details about the car being considered. The salesman is bound to give correct answers to the questions. Similarly, the brochures about the particular car model cannot make a mis-representation (tell a lie) about the model. This obligation to disclose only the truth applies when we speak of contracts of good faith.

Is the car salesman obliged to disclose (tell) everything he may know about the car? The answer is No. The buyer has to be aware of what he is buying.

Example 2: Shri Kishore aged 45 years applied for insurance on his life with policy term of 15 years. The insurer promises to pay the sum assured to the legal heirs of Kishore in case Kishore dies during the policy term. The insurer has to predict the chances of Kishore's survival over term of the insurance i.e., the next fifteen years. Can the insurer make an accurate prediction without knowing complete details about Kishore like his state of health, past diseases, family health history, habits etc. The insurer would not be in a position to know these facts unless they were completely disclosed by Kishore. Any problem in health would adversely impact the chances of survivaltill the policy term, which in turn would result in insurer paying the sum assured to the claimants of Kishore. Thus,the cost of insurance is more for insurer in case the ill-health of insured is not disclosed. Imagine the policy sold has special features and conditionslisted in the policy document. Can Kishore know about these features and conditions unless the same are disclosed to Kishore by the insurer?

In Example 1 above, while the buyer of the car can see, touch and test-drive the car, the purchaser of insurance gets only a promise that he or claimants on his behalf would be paid an amount when something happens.

On the other hand, the seller of the car clearly knows whatheis selling and what his costs are in manufacturing the car. In the case of the insurer (Example 2), when he is entering into a contract, he is able to quess (estimate) the chance of the loss and the amountof the loss that may happen (which would be huge compared to the premium collected) based on his knowledge of the ‘risk’ that he is accepting. Here, we should note that when an insurance contract is entered into, the insured person knows everything about the risk insured but the insurer knows nothing. The insurer can assess the probability of loss (depending on which he decides to accept the risk and charge the premium) only based on whatthe insuredtells him about the risk. Similarly, the insured would not understand what the benefits are in relation to the cost paid (premium paid) unless the same are made known to him to enable him to make an informed choice.

Insurance contracts thus stand on a different footing as compared to other kinds of commercial contracts. Disclosure of all material information has to be made by both the parties to the contract. Hence the contracts of insurance are referred to as contracts of utmost good faith. Since these contracts are based on prediction of an event (Known as a contingency), they are called as contingent contracts. The prediction depends on complete disclosure being madeofall facts that would impact the risk.

The proposerin insurance thus has a legal obligation (legal duty) to disclose everything and all material facts that are relevant to the subject-matter of insurance.

Definition

Amaterial fact is one which would affect the judgment of a prudent insurer in deciding whether to accept the risk and if so, at what rate or premium and subject to what terms and conditions.

Example

- In respect of insuring a factory, one must disclose the type of construction of the building and the nature of goods stored;

- In the case of goodsin transit (Marine Cargo insurance), the method of packing and the mode of transportation has to be disclosed.

- Inthecase of life insurance,the state of the health of those proposed for insurance, details of past ailments and the treatments done have to be disclosed.

4. Principle of indemnity

Let us understand the principle of indemnity with the help of an example.

Example

Jayesh had a shop which caught fire and as a result, a part of the goods that were stored was destroyed. The shop was insured for its full value of Rs.5,00,000. Jayesh claimed Rs. 5,00,000 since he had insured his shop for Rs. 5,00,000. The insurance company's surveyor examined the damage and estimated that the loss was only Rs. 64,000. The insurance company paid Rs.64,000 as compensation, even though Jayesh had a policy of Rs. 5,00,000 and claimed for more. The insurer was applying a law known as the “Principle of Indemnity”.

You get compensated for what you lose - no more, no less.

The principle of indemnity means that the loss, and only the loss, is compensated. Insurer has to indemnify (ie. pay for the financial loss suffered by) the insured. At the same time, the insured should not be paid anything more than the financial loss suffered by him. In other words,the insured should not be able to make a profit out of the loss suffered.

The insurance contract is for compensating the person who experiences a loss so that he is brought back to the same financial position as before the loss. The insurance policy indemnifies or guarantees compensation only for the amountofloss and for nothing more.

One should note that insurance policies have a sum insured, which indicates the total value of the risk that is taken over by the insurer through the policy.

Sum insured should be understood depending on the type of insurance as:

- Thevalue of acar,

- The value of ahouse,

- The estimated medical expenditure or

- The amount that would take care of a family's financial needs in case of the breadwinner's death.

Payment of any higher amount would normally mean a profit for the insured.

Payments for loss or damage under insurance contracts are limited to the actual amount of the loss or damage or the sum insured, which would be the maximum liability of the insurer. The purpose here is to ensure that one should not expect to make profit out of a loss through insurance.

Consider this situation

Consider a case where Mrs. X takes insurance on her life. Suppose she were to die. Would it be possible to exactly estimate the actual amount of loss or damage suffered? You would find that the above questions cannot be answered easily. The value of a person's life cannot be measured precisely.

Life insurance contracts hence follow different principle. The life insurer pays an amount that is fixed at the beginning of the contract. Such amountis known as sum assured. Thus, life insurance contracts are known as contracts of assurance rather than contracts of indemnity.

5. Subrogation and Contribution

What are subrogation and contribution?

Both principles of subrogation and contribution arise from the principle of indemnity.

a. Subrogation

Consider this situation

On his transfer from Kolkata to Mumbai, Mr.Rajan sends his household goods worth Rs.1,00,000 through M/s. Jayant Transports. During the transit, part of the goods got damaged due to the truck driver's negligence.

The insurer assessed the loss and found that the value of the damage was Rs. 30,000 and paid this amount to Mr.Rajan as indemnity. However Mr.Rajan took up the matter against M/s Jayant Transports with the Court of Law and the Court ordered M/s. Jayant Transports to pay Rs.30,000 to Mr.Rajan. Having already received Rs.30,000 from the insurer, Mr.Rajan would be making a profit out of the loss if he gets Rs.30,000/- from the transporter also.

From this situation, one should observe the following:

- The insurance company has to compensate Mr.Rajan as per the insurance contract at the earliest without making him wait for the Court's judgement.

- Mr.Rajan should not get two compensations and make a profit out of his loss.

In such situations, the insured’s right to claim from anywhere else is taken over by the insurer when he pays a claim. Since the insurer has paid the amountof loss to the insured, the insurer would be the one who has bome the loss. Hence, the name of the insurer should be substituted for the insured and the right to recover the amount of loss from the person causing loss has to be transferred to the insurer who paid for the loss and compensated the insured. This taking over of the insured's right by the insurer is called ‘subrogation’ in insurance parlance. In other words, on payment of the claim, the insured's right to claim from anywhere else gets 'subrogated' to the insurer.

In the matter of subrogation, one should be clear that the insurer's rights of subrogation are limited to the amount he has paid towardsclaims.If, in the case cited above, the Court had ordered M/s. Jayant Transports to pay Rs.50,000 (instead of Rs.30,000) to Mr.Rajan, the insurer would have subrogation rights only up to Rs.30,000 that it paid and the balance Rs.20,000 would goto Mr.Rajan.

How subrogation works

b. Contribution

Consider this situation

Mr. Kishore had a car worth Rs.5,00,000 and he took full insurance for this car from two insurance companies. The car was totally damaged in an accident and total loss was Rs.5,00,000. Mr. Kishore filed a claim with the 1st company and got paid Rs.5,00,000. He goes to the 2nd insurance company and makes a claim for Rs.5,00,000. The second company informed Mr.Kishore that he was noteligible for getting any more sum because he was already indemnified by the 1st Company.If the 2nd company had also paid him, he would have made a profit out of his loss, to the disadvantage of all the other members who had contributed premiums.

This situation is against the principle of indemnity in insurance as Mr. Kishore would be making a profit out of his loss.

The principle of contribution refers to the right of an insurer who haspaid a loss under a policy to recover a proportionate amount from other insurers who are alsoliable for the loss.

Example

If a property is insured under two fire policies each for Rs. 300,000,in the event of a partial loss of Rs.1,00,000, the insured is entitled to recoverhis full loss from any one of the insurers who, thereafter is entitled to recover from the other insurer his proportionate share i.e. Rs. 50,000. So, the different insurers under different policies contribute in indemnifying and paying for the loss caused by an insured peril.

6. Principle of proximate cause

Let us understand the principle of proximate cause with the help of an example.

Example

Mr. Prathamesh had taken an accident insurance policy which covered death by accident. While walking on the road one day, he was hit by a car. He was rushed to the hospital. Being a person with a weak heart, he could not stand the shock of the event and died after a few hours from heart failure. The insurance company disputed the claim saying it was the heart attack rather than the accident which had caused his death. The court ruled that even though the immediate cause of death may have been collapse of the heart, the proximate cause of death was the accident and ordered the company to pay the claim.

The above example is a case of a key principle in insurance, known as proximate cause. The word 'proximate' means ‘nearness’or 'closeness’. The concept is that the cause that is 'closest' (in its effect) to the loss, is considered to decide whether a claim is payable or not.

If loss to an insured property is the result of two or more causes acting simultaneously or in succession (one after another), it becomes necessary to choose the most important, the most effective or the most powerful cause which has brought about the loss. It is the active efficient cause that setsinto motion atrain of events which brings about a result, without the intervention of any other force. This cause is termed as “proximate cause’, all other causes being considered as “remote”. If the proximate cause of loss is covered under the policy, the claim becomes payable.

Your comments