The 50/30/20 Budget Rule: How to Manage Your Money Wisely

The 50/30/20 rule is a common practice used for budgeting that can help you allocate your income in a planned way. The rule simplifies the process of saving and spending by categorising your budget into three main categories: needs, wants and savings. This can help you achieve financial security for your future needs while managing your current expenses effectively.

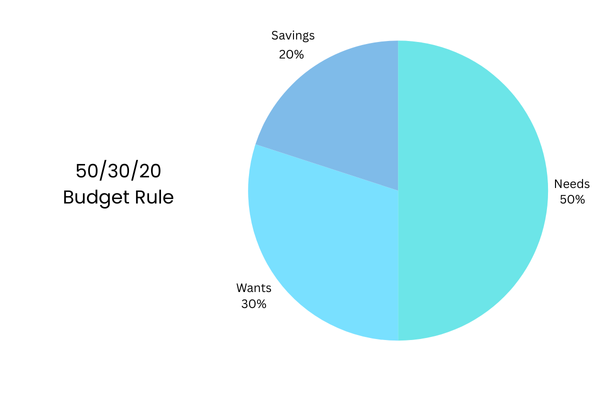

Needs: 50%

50% of the income should go towards needs. These include essential expenses such as

- Rent or mortgage payments

- Utilities (electricity, water, gas)

- Groceries

- Transportation (car payments, fuel, public transit)

- Insurance (health, auto, home)

- Minimum debt payments

- Basic healthcare and medications

Wants: 30%

30% of savings go to the wants. Wants are the things you spend money on that aren't absolutely essential. You can work out at home instead of going to the gym or watching sports on TV instead of getting tickets to the game.

This includes also upgrade decisions in life like buying a BMW from having a Suzuki or moving to a Villa from a small house etc.. Some Examples of this includes:

- Dining out

- Entertainment (movies, concerts, events)

- Hobbies and leisure activities

- Vacations and travel

- Subscription services (Netflix, Spotify, etc.)

- Shopping for non-essential items (clothing, gadgets)

- Gym memberships

- Luxury items and upgrades

Savings: 20%

The last 20% should go to the savings for future use. You should have at least three months of emergency savings on hand in case you lose your job or an unforeseen event occurs. Focus on retirement and meeting more distant financial goals after that. Examples of savings can include:

- Emergency fund

- Retirement accounts (401(k), IRA)

- Investment accounts (stocks, bonds, mutual funds)

- College savings plans (529 plan)

- High-yield savings accounts

- Paying off high-interest debt

- Health savings account (HSA)

- Real estate investments

- Certificates of deposit (CDs)

- Tax-advantaged accounts

Importance of savings

Savings are crucial for financial stability and future planning. They provide a safety net during emergencies, help in achieving long-term goals, and reduce financial stress. By saving regularly, you can ensure that you have funds available for unexpected expenses, retirement, and other significant life events. Additionally, savings can help you avoid debt and provide opportunities for investment, which can further grow your wealth over time.

How to use 50-30-20 Rule

-

Calculate your after-tax income:

Determine your monthly income after taxes and deductions. -

Allocate 50% to needs:

Identify and list your essential expenses such as rent, utilities, groceries, and transportation. -

Allocate 30% to wants:

List non-essential expenses like dining out, entertainment, and hobbies. -

Allocate 20% to savings:

Set aside money for savings, investments, and debt repayment. -

Track your spending:

Monitor your expenses regularly to ensure you are sticking to the 50-30-20 rule. -

Adjust as needed:

Review and adjust your budget periodically to accommodate changes in income or expenses.

Real-Life Examples

- Low Income ($2,000/month): $1,000 needs, $600 wants, $400 savings—tight but doable with adjustments.

- Middle Income ($5,000/month): $2,500 needs, $1,500 wants, $1,000 savings—room for comfort and growth.

- High Income ($10,000/month): $5,000 needs, $3,000 wants, $2,000 savings—luxury meets wealth-building.

- Engagement Tip: Include a table showing these scenarios for easy scanning.

Common Pitfalls (and Fixes)

- Overspending on Wants: Set a weekly cap (e.g., $50) to stay in line.

- Ignoring Irregular Expenses: Save a bit extra in the 20% bucket for surprises like car repairs.

- Not Adjusting Over Time: Revisit the budget as income or goals change.

- Engagement Tip: Bold key fixes to grab attention.

Conclusion

The 50/30/20 rule is your shortcut to financial freedom—spend wisely, save smartly, and live well.

Your comments